Okay, I admit to being a total wimp when it comes to cold weather. Waking-up to frost on the roofs and going out for a walk with gloves and a hat is not my favorite part of living in San Diego in January. But I have to tell you that my heart is warmed as soon as I turn on my computer, look at my emails, my transactions, and the MLS and realize that the San Diego real estate market is hot, hot, hot!

This is due to 4 primary factors:

1) Employment in the County in October was up by 1.9% over October 2011*

2) Consumer confidence (Pacific West) is up by 36%*

3) Interest rates remain at record lows

4) Inventory is approximately 50% of what it was a year ago*

The lack of homes to sell in San Diego County is clearly illustrated in these two graphs, which show unsold inventory at lowest point since 2005, and that homes in the $750 – $1000K range are the most scarce. However, as there are fewer people able to buy in that range the impact is less dramatic. The price range where we are feeling the greatest impact is the $300 – $500K range. If you’re a seller, you love it as you will likely have multiple offers within days of listing. If you’re a buyer, not so much, as it’s likely you’ll be in a bidding war with several cash buyers.

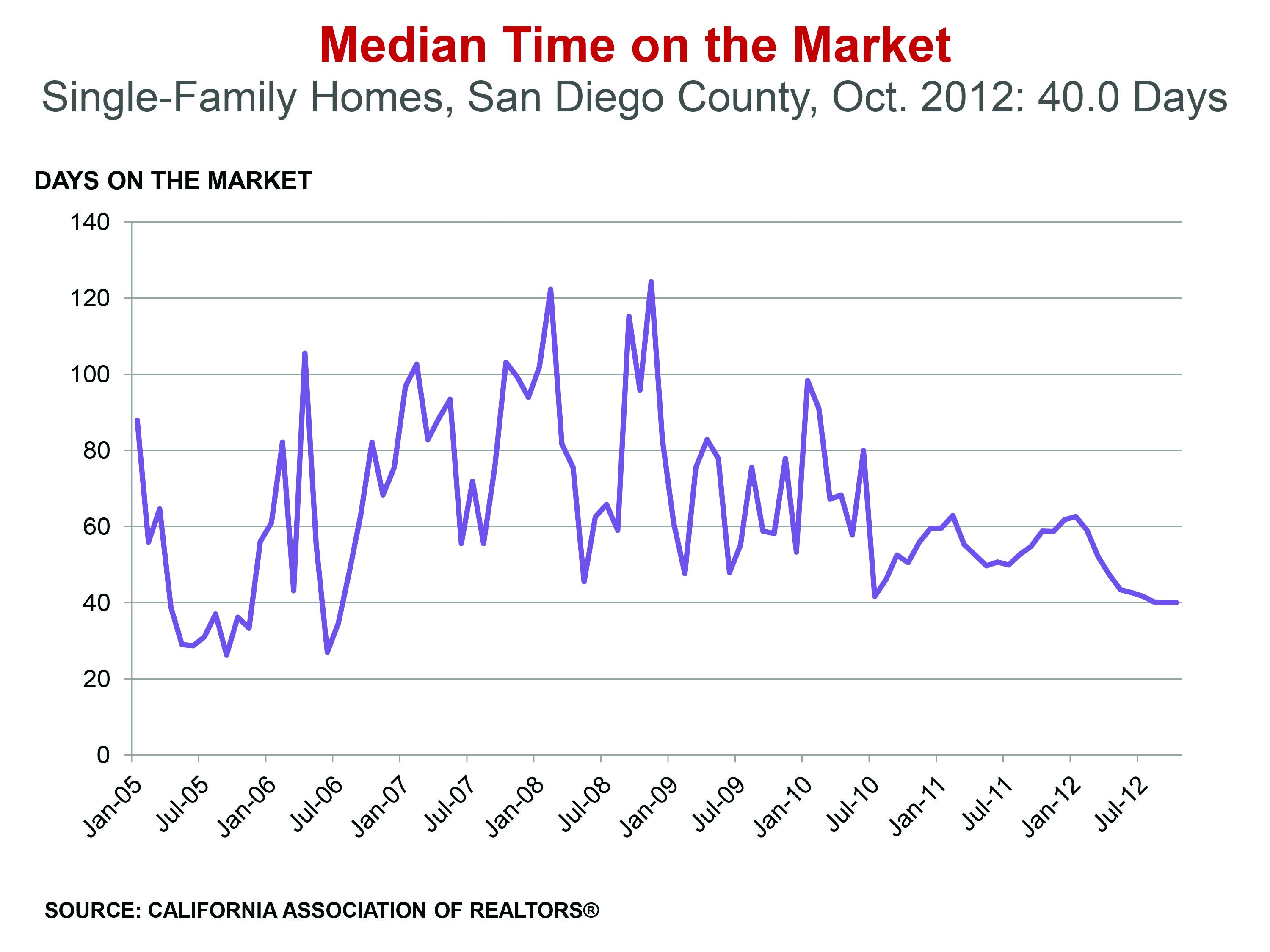

This of course has driven down the length of time homes stay on the market from approximately 60 days in January of last year to just 40 days in October.

The net result of all these factors is that prices in the San Diego real estate market are increasing at a steady rate, up 10.7% this October, over October 2011.

So is it a good time to buy or sell in San Diego? Absolutely! Barring any economic catastrophe I believe we’ll continue to see a strengthening real estate market throughout 2013. So if you’ve been considering a real estate investment, best to get in the game now as I predict prices will continue to rise. Please give me a call to discuss the opportunities available in America’s Finest City!

* Graphs and statistics courtesy of the California Association of Realtors®. All statistics reflect sales activity for detached homes.